Orion Farming Group Weekly Straights Update: 23rd April 2026

- Orion Farming Group

- Apr 23

- 3 min read

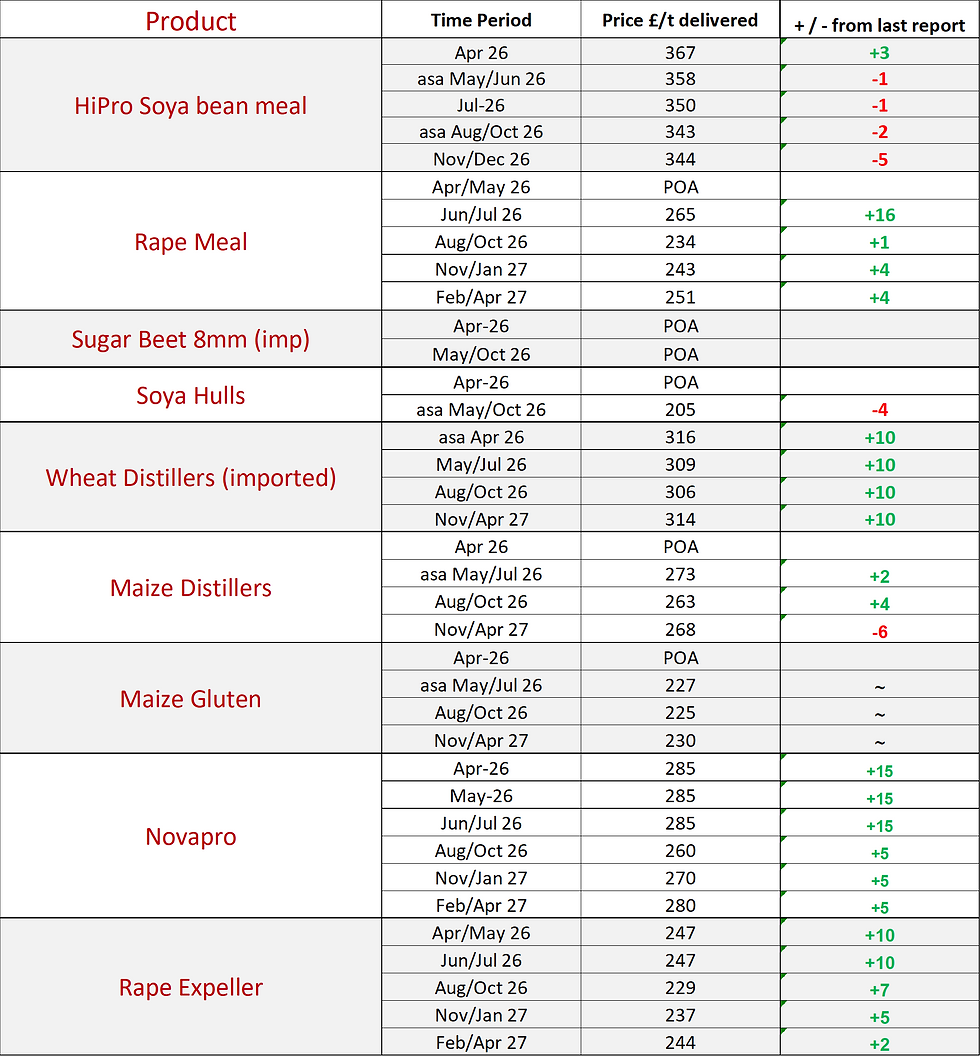

The figures in the charts are an indication only and reflect levels traded on Wednesday.

Click on a product name for more information

Prices have stayed steady nearby as the US market took a breather.

They remain at a premium to forward prices as the Argentinian harvest continues to be delayed by rains, as well as driver protests in parts of the country, which is further hampering exports.

Forward prices have eased somewhat as there is some risk off approach from a geopolitical POV given the plentiful supply there is, globally.

Nearby looks unlikely to ease much due to the tight UK supply and increased demand due to the lack of rapemeal.

Soybean futures have remained rangebound for the last few weeks due to uncertainty around future demand for US beans ahead of talks between the US and China in May.

Concerns linger as to how these talks will pan out as a result of China being negatively impacted by the closure of the Straits of Hormuz, so they may not be in a generous mood for further deals with the US.

US planting is now at 7% complete slightly ahead of the average due to dry conditions.

Chinese imports were down 3% vs last year for the Jan/Mar period showing signs that they are looking to reduce their reliance on imports, either with higher domestic production or alternative feed products.

Supply into May is very tight with any offer significantly higher than a few weeks ago.

Most shippers are now not sellers until their next shipments due mid-May and June.

This is as a result of Erith not reopening yet and so having to buy additional product each week to supply some of their contracts.

Old crop values now sit at about 78% of the soya price for spot/May and 70% Jun/Jul, so it doesn’t look great value for those who can switch proteins.

The rapeseed complex (seed/meal/oil) had a rally towards the end of last week as the European market became wary of Erith not reopening in the near future.

This would leave a much tighter picture for May/Jul supplies that had previously been priced, so the market moved higher as a result.

New crop prices are thought to be in better stead so the rally didn’t push forward prices as high, (Erith still sitting circa 65% of soya prices and Liverpool 72%).

Nearby supply seems to have improved a little as well as forward summer prices moving down due to more confidence in the decent crops out of South America.

Further price drops may be limited by the domestic demand in Argentina and also other export markets who are prepared to pay these values.

Prices for the next couple of months have eased back as some Ensus material is now being offered, though August onwards remains steadier due to uncertainty as to whether Ensus will remain open beyond Jun/Jul, so pricing is based on imported product.

Imported product is still at a premium due to lower exports from the US as mentioned in previous reports.

Wheat distillers are roughly £15/T premium vs maize distillers for the summer.

Another week of an unchanged market with no prices offered for the summer – either home produced or imported.

The wheat market was still mixed as it continued to weigh up rains in the US and ample global supplies vs geopolitical risks.

Rains in the US have come through but not in all regions, so drought conditions remain.

Also large stocks in Europe and strong competition from the Black Sea are keeping some limits on prices.

There is also beginning to be some talk of lower planted areas for future crops due to higher energy and fertiliser costs.

Overall barley remains tighter in the UK, with strong demand throughout the winter.

And finally, totally irrelevant but quite interesting facts of the week…….Quidditch, digestive biscuits and overdrafts were all invented in Edinburgh and the phrase ‘survival of the fittest’ was coined by Herbert Spencer, not Charles Darwin.

Notes:

All figures in this report are provided by KW and commentary by GLW Feeds. Price indications are based on 29t bulk tipped loads delivered to Oxfordshire and are guide prices only.

For firm prices and availability, please contact Joe Cobb on 01865 393 139

Currency Trends as of 15.04.26 Blue = GBP:USD. Red = GBP:EUR